Signing of the New Tax Convention between Japan and the Republic of the Philippines

28 May 2026

The Ministry of Foreign Affairs of Japan, on 28 May 2026 published the new double taxation agreement (DTA) between Japan and the Republic of the Philippines. The new DTA wholly amends the existing Convention, which initially entered into force on 20 July 1980 and was partially amended on 5 December 2008.

Among other changes, the new DTA introduces measures to prevent abuse of the DTA, arbitration proceedings within the framework of mutual agreement procedures and assistance in the collection of tax claims and strengthens the exchange of information of the contracting states in respect of tax matters.

From an investment perspective, the DTA introduces updated provisions on taxation on business profits and investment income (dividends, interest and royalties).

KEY PROVISIONS:

1. Business Profits

- A company is taxed in the other country only if it has a “permanent establishment” (e.g., branch).

- Profits taxed are only those attributable to that establishment, based on the arm’s length principle.

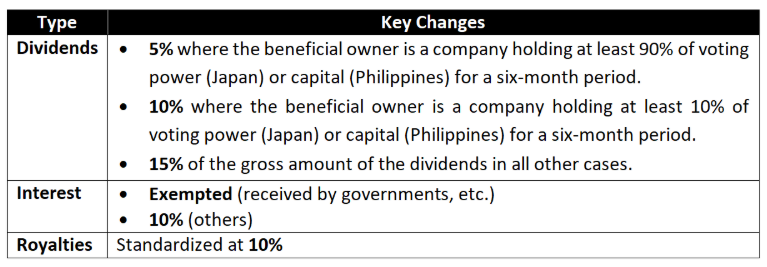

2. Investment Income (Dividends, Interest, Royalties

- Overall, the agreement lowers or harmonizes tax rates to promote cross-border investment.

3. Mutual Agreement Procedure and Arbitration Proceedings

- Countries will first try to resolve tax disputes through mutual agreement procedures.

- If unresolved after 2 years, cases can go to arbitration.

4. Exchange of Information and Assistance in Collection of Tax Claims

- Expands exchange of tax information between Japan and the Philippines.

- Introduces mutual assistance in tax collection (a major upgrade from the old treaty).

5. Prevention of Abuse of the New Convention

- Prevents misuse of treaty benefits:

- If a transaction’s main purpose is to gain tax benefits, those benefits may be denied.

6. Effectivity of the new Tax Treaty

- Must be approved domestically (e.g., Japan’s Diet).

- Enters into force:

- 30 days after both countries complete approval.

- Applies starting:

- January 1 of the following year after entry into force.

Source:

https://www.mof.go.jp/english/policy/tax_policy/tax_conventions/press_release/20260528phl_pt.html

For any assistance or inquiry, you may contact us through the contact details below:

+632.8982.9100

info@reyestacandong.com

You may access the full version of the Japan-PH Tax Convention through this link

Contact us today. We’ll schedule a complimentary assessment of your company.

Let RT&Co help your business. Send your request for a proposal of services here.