BIR Issuances – RMO No. 17-2025

Share this article

Revenue Memorandum Order No. 38-2025

Date Posted (BIR Website): September 8, 2025

Effectivity: Apply prospectively to all claims for excise tax refund on petroleum products filed on April 1, 2025 onwards

Consolidated Guidelines and Procedures for the Processing of Claims for Refund of Excise Tax Paid on Petroleum Products

I. Background

- RMO 16-2024 sets documentary requirements and procedures for excise tax refund claims on petroleum products.

- With new laws — TRAIN Law (RA 10963), EOPT Act (RA 11976), and CREATE MORE Act (RA 12066) — revisions were made to Sec. 135 and the introduction of Sec. 135-A of the Tax Code.

- Updates are needed to streamline refund claims for excise tax paid on petroleum products sold to international carriers and exempt entities/agencies.

II. Objectives

- Amend provisions of RMO 16-2024, including the updated checklist of required documents.

- Provide consolidated, uniform guidelines and procedures for processing claims filed with RDOs and Large Taxpayers Service (LTS).

III. General Policies

- Basic Requisites for refund claims under Secs. 135 & 135-A:

• Filed within 2 years after payment of tax/penalty.

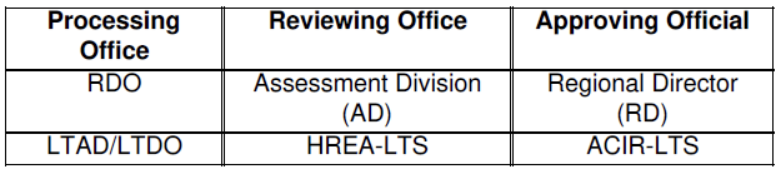

• Must use BIR Form No. 1914 with proof of payment (BIR/BOC). - Authorized Processing Offices:

• RDOs

• LTS (LTAD/LTDO) - Roles:

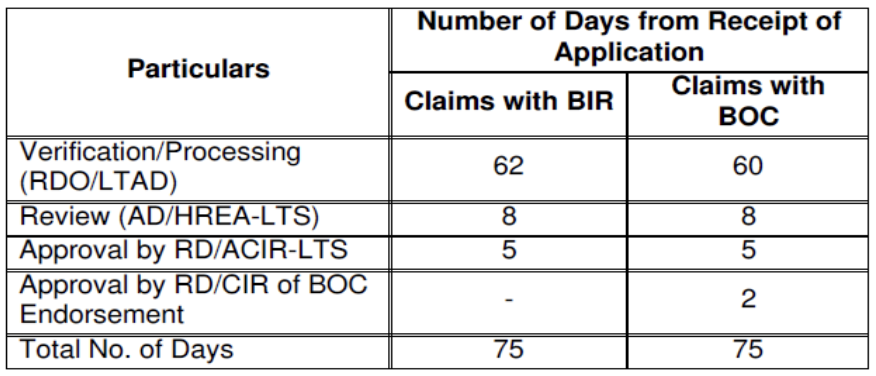

- 90-Day Rule: Refunds must be granted/denied within 90 days of complete submission. Hence, the offices concerned shall strictly observe the 90-day time frame to grant in full or in part the claims for refund, broken down as follows:

- Refund Payment Processing:

• Regional Offices: max 15 days after approval.

• LTS: max 15 days after approval.

- Claims must be filed quarterly, aligned with the taxpayer’s accounting period.

- Documentation:

• Application letter + BIR Form 1914;

• Secretary’s Certificate;

• SEC registration;

• Audited FS / books;

• Sworn Statement (Annex A-1);

• Excise tax returns (BIR Form 2200-P) + proof of payment;

• Withdrawal Certificates, invoices marked “no excise tax”;

• ORBs (Official Register Books) in CSV and printed form;

• Importation documents (SAD, SSDT, ATRIG, invoices, etc., for importers); and

• Certificates from DFA, CAB, IMO, BOC, and regulatory authorities (depending on the type of exempt buyer). - Refunds only apply if excise taxes were not passed on to customers or recorded as deductible expenses.

IV. Procedures

- Processing Office (RDO/LTAD):

- Initial check, issue Tax Verification Notice (TVN), verify books and records, prepare report and recommendation.

- Reviewing Office (AD/HREA-LTS):

- Ensure legal basis, accuracy, and completeness of claims.

- Approving Office (RD/ACIR-LTS):

- Approves or denies refund; signs supporting documents.

- Payment:

- Finance & Accounting divisions process refund vouchers; Administrative Service issues refund checks.

- Coordination with BOC:

- Approved claims involving imports endorsed to BOC with supporting documents.

- Reporting & Safekeeping:

- Monthly reporting to the BIR Assessment Service.

- Approved claims’ dockets → COA; denied claims → filed in RDO/LTS records.

V. Effectivity

- Applies prospectively to all claims filed April 1, 2025, onwards.

- Claims filed before this date → governed by RMO 16-2024.

You may access the full version of this RMC and related Annexes through the links below.

Contact us today. We’ll schedule a complimentary assessment of your company.

Let RT&Co help your business. Send your request for a proposal of services here.