RT&Co. Market Update | The Philippine Economy Amid the Lingering Energy Crisis: Where Are We Now?

Executive Summary

More than six months after the onset of the Gulf conflict, the Philippine economy continues to operate with elevated energy costs, persistent inflation, supply chain uncertainty, and heightened geopolitical risk. The initial shock to global energy flows has eased, but the effects remain visible in freight, insurance, commodity prices, and business operating costs.

The important point is that the adjustment has not been uniform. Recent data and corporate disclosures point to a more differentiated economy: some industries remain resilient, some are reallocating resources, and others are beginning to show clearer signs of strain. This distinction matters because it offers a better read of business conditions than headline macroeconomic indicators alone.

This update uses that distinction to assess where the economy appears to be in the adjustment cycle, which sectors are absorbing the pressure, and what signals should be monitored through the remainder of 2026.

Where Are We Now?

Several macroeconomic indicators suggest that the Philippine economy remains under sustained external pressure.

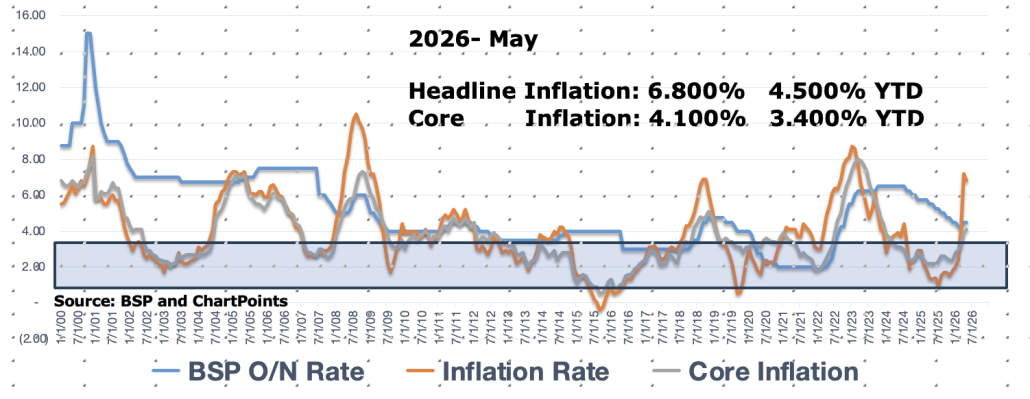

Headline inflation for May stood at 6.80% above the Bangko Sentral ng Pilipinas’ upper target rate of 4.00%, with transport and food still accounting for a meaningful share of price increases. Gross International Reserves have declined from their all-time peak of US$112.72 billion in February 2026 to US$104.0 billion in May. The Government has also moved to strengthen energy security through initiatives such as strategic petroleum reserve planning, diversification of crude oil sourcing, and faster deployment of renewable energy capacity.

Figure 1 Inflation trends in the Philippines

Globally, energy markets have improved from the most acute phase of the Gulf conflict but have not returned to pre-crisis conditions. Volatility in energy prices, freight, insurance, and logistics continues to feed into Philippine business costs through imported inflation and higher operating expenses.

The economy has therefore moved from immediate crisis response into a more prolonged period of adjustment.

This is broadly consistent with the Asian Development Bank’s Philippines outlook, which continues to frame the economy as supported by domestic demand and investment but exposed to downside risks from inflation, external uncertainty, and energy-related cost pressures.

A Working Lens for Reading the Market

For purposes of this update, we are using a simple working lens to make sense of events as they unfold. Demand destruction – the point where overall consumption, investment, or activity begins to fall – usually does not happen immediately. It tends to appear only after businesses and households have first tried to absorb higher costs, adjust spending, and reallocate resources.

This view is broadly consistent with the work of economists such as James D. Hamilton, Lutz Kilian, Christiane Baumeister, Gert Peersman, and others who have studied oil shocks, commodity shocks, and their effects on economic activity.

Using that lens, the current environment can be read in four broad phases:

- External shock: energy and commodity disruption raise costs and uncertainty.

- Absorption: businesses and households manage the pressure through pricing, cost control, inventory decisions, substitution, and operating efficiencies.

- Reallocation: spending shifts across products, brands, sectors, and channels rather than disappearing altogether.

- Demand destruction: if the pressure persists, overall purchasing volumes, investment, hiring, and economic activity may begin to weaken.

The purpose is not to present a forecast model, but to provide a practical way to distinguish between temporary adjustment, shifting demand, and more durable demand weakness.

Evidence of an Uneven Economy

The sector evidence supports the view that the economy is not weakening in a straight line. Instead, the pattern is one of resilience in essential and energy-related activities, greater selectivity in consumer and property decisions, and sharper pressure in sectors directly exposed to fuel and travel costs.

A similar pattern appears in recent Southeast Asia market commentary, which describes growth across the region as increasingly divergent, with domestic demand remaining supportive in some economies and sectors while cost pressures and external headwinds expose weaker areas. This regional framing supports reading the Philippine evidence as an uneven adjustment rather than a single broad-based downturn.

Energy and Power

Selected SEC/PSE filings and company disclosures indicate that large integrated electricity businesses with significant generation portfolios have generally reported resilient earnings during the first half of 2026. The available disclosures point to support from power generation, renewable energy assets, and contracted capacity, even where regulated distribution volumes have softened modestly.

Interest in renewable energy, solar, battery storage, and energy-efficiency solutions has also increased as businesses seek to reduce long-term exposure to imported fuels and electricity price volatility.

The observable response has been one of accelerated investment in energy resilience rather than defensive retrenchment.

Consumer Staples and Everyday Consumption

In consumer markets, the strongest performance remains concentrated in everyday spending.

Selected SEC/PSE filings indicate that major retail operators continue to show resilience in supermarket and neighborhood retail formats, although profitability has been more mixed because of financing costs, operating costs, and softer consumer confidence. Some quick-service restaurant and food-service operators have also continued to report sales growth despite higher food and commodity costs, presumably relying on disciplined pricing, menu optimization, and product mix rather than aggressive discounting.

Other consumer categories, including tobacco and alcoholic beverages, should be read more selectively. Resilience may be present in some companies, but the evidence is best assessed through company-specific filings rather than broad sector generalization.

The observable response across these sectors has been disciplined cost management while preserving customer traffic and market share.

Property

Property shows a clearer split between recurring income and large-ticket commitments. Selected property-company filings show continued support from shopping malls, office leasing, commercial operations, and hospitality, while residential development revenues and sales reservations have weakened in some disclosures.

This does not necessarily indicate broad consumer weakness. It suggests that households are becoming more selective, maintaining everyday expenditure while exercising more caution on major financial commitments.

Transportation, Tourism and Hospitality

Transportation and tourism remain among the sectors most directly exposed to the continuing energy crisis.

Airline route suspensions, reduced flight frequencies, higher fuel surcharges, and weaker tourism activity in some destinations indicate that higher aviation fuel prices and operating expenses have begun to translate into route rationalization, operating adjustments, and pressure on discretionary travel.

Here, the observable response has shifted beyond cost management toward operational restructuring.

Manufacturing

Manufacturing remains mixed. Selected SEC/PSE filings and management discussions suggest that some companies are adapting through procurement management, product mix adjustments, operating efficiencies, inventory management, and selective pricing actions. The evidence, however, remains company-specific rather than a uniform sector-wide trend.

These responses suggest that much of the sector remains in the absorption phase rather than experiencing broad demand contraction.

A Common Theme: Reallocation Rather Than Collapse

Taken together, current evidence suggests that Philippine consumers continue to spend, but they are spending differently.

Rather than exhibiting widespread withdrawal from consumption, households appear to be reallocating expenditure toward essential goods, familiar brands, value-oriented offerings, and recurring consumption while showing greater caution toward travel, residential property, and other large discretionary commitments.

Corporate disclosures reinforce this observation. Across multiple industries, management teams continue to focus on pricing discipline, operating efficiency, product mix, procurement management, and energy management rather than broad restructuring or capacity reductions.

At present, the available evidence appears more consistent with demand reallocation than with generalized demand destruction.

What to Watch During the Second Half of 2026

Prolonged commodity and energy shocks do not normally translate into broad-based demand destruction immediately. They usually pass through a period of absorption and reallocation before more durable weakness appears.

Accordingly, the indicators most likely to provide early evidence of a transition toward demand destruction include:

- sustained declines in unit sales despite stable revenue growth;

- increasing down-trading toward lower-priced products and services;

- weakening residential property reservations and large-ticket consumer purchases;

- deteriorating occupancy or leasing demand in commercial property;

- increasing customer receivable days and signs of consumer credit stress;

- weakening export-oriented manufacturing activity, particularly in electronics;

- slowing remittance inflows from the Gulf region;

- continued pressure on the country’s external accounts, including foreign exchange reserves and the peso.

These indicators should be viewed collectively rather than individually. Their value lies in showing whether the economy is moving beyond adaptation and reallocation into a more sustained reduction in aggregate demand.

For boards and management teams, this distinction is critical. The central question for the remainder of 2026 is no longer whether businesses are operating under pressure; they clearly are. The more important question is whether current adaptive strategies remain sufficient, or whether they begin to give way to measurable demand destruction. The answer will shape decisions on capital allocation, pricing, workforce planning, liquidity management, and business continuity well into 2027.

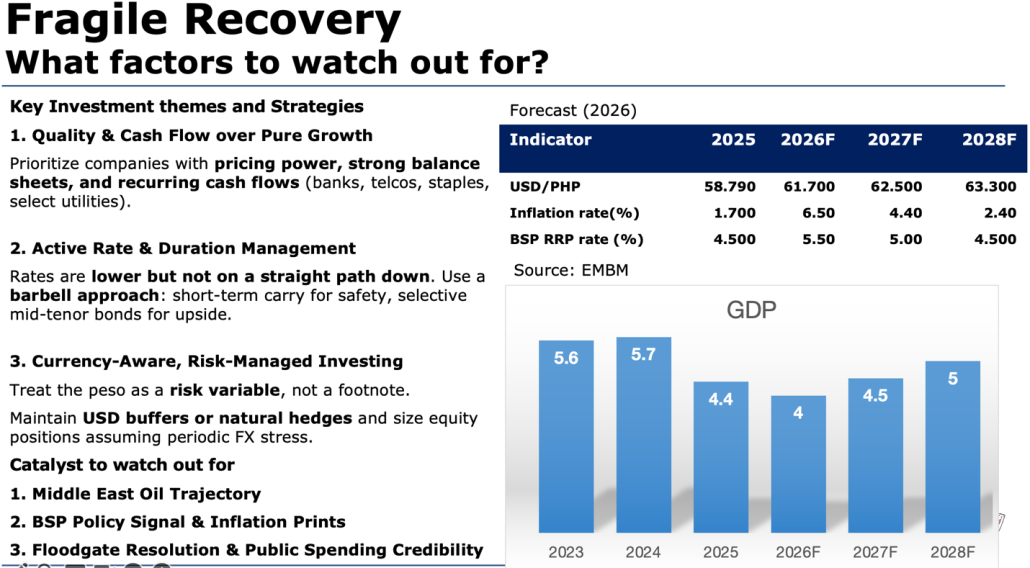

Figure 2 What to Watch Out For and Some Tactical Responses

Figure 2 maps key economic trends over the next six months and provides a practical starting point for adaptive strategy. For instance, this suggests some liquidity management responses that may still be sufficient under an absorption or reallocation scenario but which may need to shift if conditions begin to move toward more durable demand weakness.

Executive Takeaway

The Philippine economy appears to be moving from cost absorption toward selective demand reallocation. Consumers continue to spend but are becoming more value conscious, while firms are prioritizing productivity, energy resilience, and operational efficiency. Current evidence suggests adaptation rather than broad-based demand destruction, although prolonged energy and commodity pressures remain the key risk to monitor during 2H 2026.

Reference basis: The observations in this market update are based on publicly available economic data, government statements, business news, SEC/PSE filings available as of publication, and selected regional macroeconomic and market commentary, including recent Southeast Asia analysis by McKinsey and the Asian Development Bank’s Philippines outlook.

The authors

Caesar “Boboy” Parlade is the Managing Partner for Advisory and Digital Transformation at Reyes Tacandong & Co. A certified public accountant and certified process management professional. He is a recognized expert in business transformation, organizational design, change leadership, digital innovation, and strategy execution. He previously held senior leadership roles in regional banking across Asia-Pacific and co-founded a Philippine shared services center for a German bank. He is a Hubert H. Humphrey Fellow in Banking at Boston University and a graduate of the Strategic Business Economics Program at the University of Asia and the Pacific.

Jonathan “Jonas” L. Ravelas, is one of the Philippines’ most respected analysts and market strategists. He is senior adviser at Reyes Tacandong & Co., and independent director at PH Resorts Group Holdings Inc. and DITO CME. For over 20 years, he was chief market strategist at BDO Unibank. A certified technical analyst, he combines data-driven precision with strategic foresight, making him a trusted voice in Southeast Asia and global economic fora.

Author

Caesar “Boboy” Parlade

Managing Partner for Advisory and Digital Transformation, Reyes Tacandong & Co.

Jonathan “Jonas” L. Ravelas

Senior Adviser, Reyes Tacandong & Co.

Contact us today. We’ll schedule a complimentary assessment of your company.

Let RT&Co help your business. Send your request for a proposal of services here.