RT ThinkTax

RT ThinkTax is our official monthly publication which highlights select and significant issuances and advisories of various government agencies including the DOF, BIR, SEC, BOC, FIRB, PEZA, and other regulatory bodies.

This RT ThinkTax Issue covers select, and significant issuances and advisories issued or published in February 2024 to present.

BIR Issuances

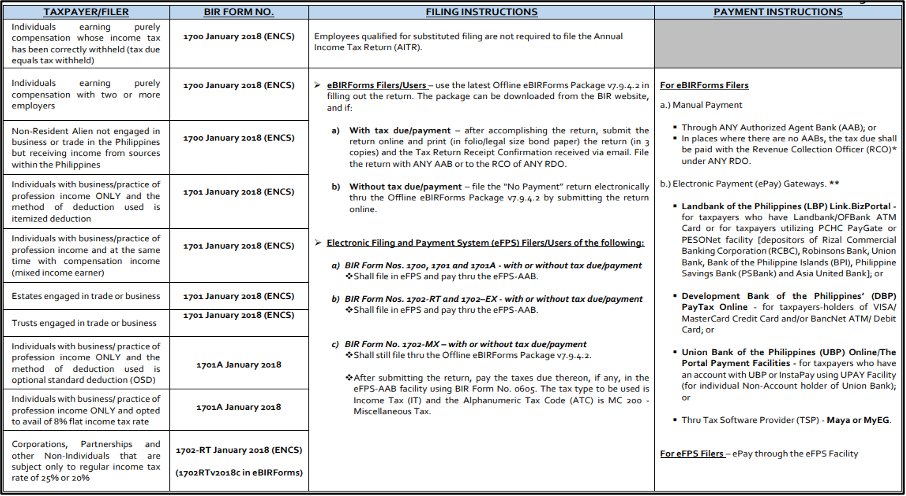

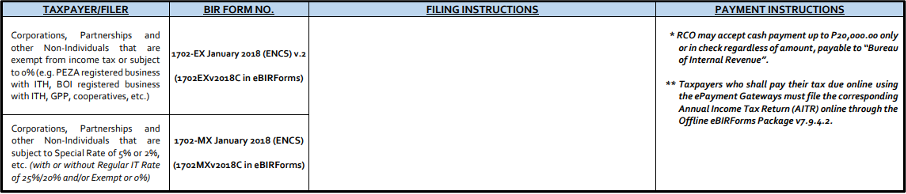

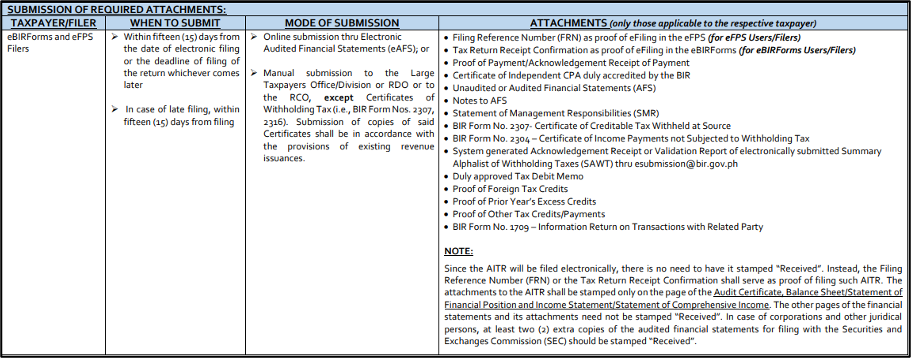

Guidelines in the Filing of Annual Income Tax Returns (AITR) and Payment of Taxes Due Thereon for Calendar Year 2023

Revenue Memorandum Circular (RMC) No. 51-2024

Issued on April 8, 2024

The filing of the AITR for Calendar Year 2023 (CY) shall be done electronically in any of the BIR electronic platforms (eFPS or eBIRForms). In case of unavailability/inaccessibility of these platforms, manual filing may be allowed.

For payment of the income tax due, it shall be made either electronically in any of the available electronic (ePay) gateways or manually to any authorized agent bank (AAB) or Revenue Collection Officer (RCO) of any Revenue District Office (RDO).

All individual taxpayers, regardless of classification, shall use the existing version of BIR Forms No. 1701 or 1701A, whichever is applicable, in the filing of the 2023 AITR. The 2-page return provided under Republic Act (RA) No. 1176 (Ease of Paying Taxes or EOPT) Act shall be used in the filing of the 2024 AITR, which is due next year (on or before April 15, 2025).

The RMC provides for the following summary:

Obligation of Authorized Agent Banks (AABs) on the acceptance of Internal Revenue Taxes for the period April 1-15, 2024

Bank Bulletin No. 2024-01

Issued on February 20, 2024

AABs shall open and accept the tax returns/payments for the period April 1 to April 15, 2024, including two (2) Saturdays (i.e. April 6, 2024, and April 13, 2024), and to extend the banking hours up to 5:00 P.M.

All income tax payments that will be accepted on April 6 and 13, 2024, shall be reported in the Batch Control Sheet as collection for the following working day, April 8, 2024, and April 15, 2024, respectively.

Acceptance of Tax Returns/Payment Forms by Authorized Agent Banks in Compliance with Republic Act No. 11976 or the Ease of Paying Taxes Act

Bank Bulletin No. 2024-02

Issued on April 1, 2024

All AABs are advised to accept all printed copies of electronically filed tax returns/payment forms thru eBIRForms and the corresponding payment of taxes due thereon from taxpayers, notwithstanding the Revenue District Office’s jurisdiction.

Announces the availability of BIR Form No. 1701 in eFPS

Revenue Memorandum Circular (RMC) No. 39-2024

Issued on March 18, 2024

This Circular is issued to announce the availability of BIR Form No. 1701 [Annual Income Tax Return for Individuals (including Mixed Income Earners), Estates and Trusts] in the eFPS

BIR Form No. 1701 shall be filed on or before April 15 of each year, covering income for the preceding taxable year.

eFPS users/filers who are mandated and required to file the said return and pay the corresponding tax due thereon, if any, shall use the eFPS Facility effective immediately.

eFPS users/filers who already filed their BIR Form No. 1701 for the taxable year 2023 using eBIRForms Facility need not re-file the return in the eFPS.

Advises all employers that the BIR does not require newly hired employees to verify their Tax Identification Number (TIN) and get a TIN Verification Slip from the Revenue District Offices (RDOs)

RMC No. 31-2024

Issued on February 27, 2024

This Circular provides that RDOs shall neither accept requests for manual TIN Verification nor issue TIN Verification Slips for employment purposes, except for the following cases:

- Online TIN Verification facility is not available, or there is a prompt message that the user needs to visit the RDO;

- A need for BIR personnel to further verify the correctness of taxpayer registration information;

- Taxpayer has an existing TIN or record; or

- Possession of multiple or identical TINs

Employers are advised to use Online Registration and Update System (ORUS) or BIR Chatbot Revie, to verify the validity and correct ownership of the TIN of their newly hired employees

Verification result displayed by ORUS is considered sufficient for verification purposes.

Employers do not have to require newly hired employees to go to the RDO to get a TIN Verification Slip

Announces the availability of additional functionalities of the Contact Center Solution and Chatbot Revie

RMC No. 33-2024

Issued on February 29, 2024

This Circular provides the additional functionalities of the Contact Center Solution and Chatbot Revie which include the following:

- eAppointment—an online appointment booking system that can be accessed through Chatbot Revie;

- Optimized Revie—Chatbot Revie was made interactive to make it more responsive to taxpayers’ queries raised through chats;

- Enhanced eComplaint Monitoring System—monitors, consolidates and generates reports of all complaints received by the BIR from various complaint channels (i.e., 8888 Citizens’ Complaint Center, Presidential Action Center, Anti-Red Tape Authority, DOF Hotline 8888, DTI, BIR eComplaint NO-OR, Contact Center ng Bayan and contact_us@bir.gov.ph);

- Live Agent Co-Browse Functionality—enables taxpayers calling the BIR Hotline No. (02) 8538-3200 a visual step-by-step walkthrough on the tax return/form/eService they are using by sharing their desktop screen with the Agent during a call (Refer to Annex A of the Circular for the procedure)

Policies and guidelines for brand registration and the submission of packaging labels and product composition/formulation sheet as an additional requirement for proper tax classification of Vapor Products pursuant to Section 4 (C) of Revenue Regulations No. 14-2022

RMC No. 35-2024

Issued on March 6, 2024

This Circular provides for the following guidelines and procedures:

- Applications for brand registration shall be accompanied by a product composition/formulation sheet indicating the specific type of nicotine used, i.e., nicotine salt/salt nicotine or freebase nicotine and affidavit signed by the chemist/pharmacist;

- The product composition/formulation sheet shall be signed by a chemist or pharmacist with his/her license number (country where applicable) following the prescribed format in Annex A;

- The sheet shall be considered final once submitted to Excise LT Regulatory Division;

- No revision on the submitted packaging labels may be allowed except for the following reasons:

- Update of graphic health warning (GHW) templates as required by the Department of Health;

- Change of registered address supported by an amended/updated BIR Certificate of Registration (Form No. 2303)

- No withdrawal of the previously submitted packaging label and product composition/formulation sheet shall be allowed.

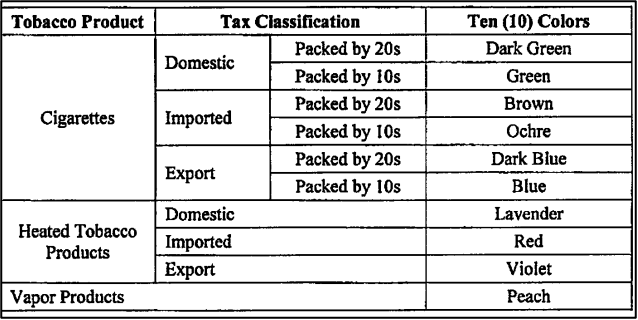

New and upgraded Internal Revenue Stamp design for cigarettes, heated tobacco products, and vapor products

RMC No. 40-2024

Issued on March 18, 2024

The new classification of the internal revenue stamps shall be as follows:

The implementation of the new and upgraded internal revenue stamp design shall take effect on June 1, 2024.

Publishes the updated list of registered manufacturers/importers/exporters of cigarettes, heated tobacco products, vapor products and novel tobacco products with the corresponding product brands/variants and integration of the requirements for compliance purposes

RMC No. 46-2024

Issued on April 1, 2024

The Circular publishes the updated list of registered manufacturers/importers/exporters of cigarettes, heated tobacco products, vapor products and novel tobacco products with the corresponding product brands/variants as of March 8, 2024.

Newly registered manufacturers/importers of cigarettes, heated tobacco products, vapor products and novel tobacco products after March 8, 2024 shall be included in the next updated list of such entities. The manufacturers/importers of cigarettes, heated tobacco products, vapor products and novel tobacco products must comply with the requisite registration of brands and variants within six (6) months from the date of release of this circular to avoid penalties.

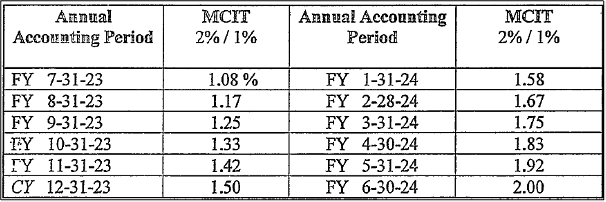

Clarifies the manner of computing the Minimum Corporate Income Tax (MCIT) for Taxable Year 2023

RMC No. 36-2024

Issued on March 11, 2024

This Circular states that Republic Act No. 11534 or the “Corporate Recovery and Tax Incentives for Enterprises Act”, prescribed the One Percent (1%) MCIT for the period July 1, 2020 until June 30, 2023. Thus, effective July 1, 2023, the MCIT rate returned to its old rate of Two Percent (2%), based on the gross income of the corporation.

In computing the MCIT, the gross income shall be divided by 12 months to get the average monthly gross income and apply the rate of:

- 1% for the period January 1 to June 30, 2023; and

- 2% for the period July 1 to December 31, 2023

For ease of computation, the rates below corresponding to the taxable period of the taxpayer may be used:

Announces the availability of TIN inquiry through electronic mail

RMC No. 37-2024

Issued on March 14, 2024

This Circular states that Taxpayers can now inquire on their TIN by sending an email at tin.inquiry@bir.gov.ph

- Procedure for Individual Taxpayers

- Accomplish the required form (Annex “A”);

- Take a “selfie” with a valid government-issued ID, and a separate photo of the valid government-issued ID, which should show the birthday and photo of the taxpayer; and

- Send the accomplished form via email to inquiry@bir.gov.ph, together with the “selfie” and separate photo of the valid government-issued ID

- Procedure for Non-Individual Taxpayers

- Accomplish the required form (Annex “B”);

- Send the accomplished form via email to inquiry@bir.gov.ph, together with the following documents:

- Scanned copy of notarized board resolution or secretary’s certificate, indicating the name of the authorized representative and the reason for the TIN inquiry;

- “Selfie” with a valid government-issued ID of both the authorized representative and authorizing official;

- Separate photo of the valid government-issued IDs of both the authorized representative and authorizing official

Clarifies the issues raised on RMC 5-2024

RMC No. 38-2024

Issued on March 15, 2024

This Circular clarifies certain pronouncements by the BIR in RMC No. 5-2024 or the circular Clarifying the Proper Tax Treatment of Cross-Border Services in light of the Supreme Court En Banc Decision in Aces Philippines Cellular Satellite Corp. v. Commissioner of Internal Revenue, GR. No. 226680, dated August 30,2022.

Some of the salient clarifications are as follows:

Q: Does the ruling in Aces Philippines Cellular Satellite Corp. v Commissioner of Internal Revenue, finding that the source of income of the Satellite Air Time Purchase Agreement between Aces Bermuda and Aces Philippines to be within the Philippines and, thus, subject to income tax, automatically apply to cross-border service agreements listed in Question No. 2 of RMC No. 5-2024?

A: No. The list of cross-border services in Question 2 of RMC No. 5-2024 (i.e. consulting services, telecommunications, etc.) was only meant to highlight that those services are performed, rendered, delivered, or supplied by a non-resident foreign corporation (NRFC).

The determination on whether the source of income of the listed cross-border services is within the Philippines is found in Question No. 3 of RMC No. 5-2024, which states that “the source of income is in the Philippines if the property, activity, or service that produces the income is in the Philippines. The flow of wealth proceeded from, and occurred within the Philippine territory, enjoying the protection accorded by the Philippine government.”

Q: Do the principles laid down in RMC No. 5-2024 run counter to the rules on the source of income under Section 42 of the National Internal Revenue Code of 1997, as amended (Tax Code)?

A: No. Question No. 3 of RMC No. 5-2024 spelled out the main guideline in determining the source of income for cross-border services, which is “the source of income is in the Philippines if the property, activity, or service that produces the income is in the Philippines. The flow of wealth proceeded from, and occurred within the Philippine territory, enjoying the protection accorded by the Philippine government”.

The rule on recognizing income under Sections 42(A)(3) and (C)(3) of the Tax Code for labor or personal service is where the labor or service is performed.

But in Aces Philippines, the Supreme Court held that “in ascertaining the income source, we must inquire into the property, activity, or service that produced the income, or where the inflow of wealth originated” and that “the subject may only be regarded as an income source if the particular property, activity or service causes an increase in economic benefits”.

Following the ruling in Aces Philippines, “the situs of the source of income for labor or personal service is not just the location, but more importantly, the location of the service that produces the income or where the inflow of wealth originates”.

Q: If it is established that the source of income of cross-border services is within the Philippines, applying the rule that the source of income is the location of the property, activity, or service that produces the income, will the subject transaction be also subject to VAT?

A: Yes. Sections 105 and 108 of the Tax Code provide that services rendered or performed in the Philippines by non-resident foreign persons are subject to VAT.

Prescribes the policies and procedures in the proper manner of accomplishing the new version of the Monthly Documentary Stamp Tax (DST) Declaration/Return (BIR Form No. 2000 version 2018)

RMC No. 48-2024

Issued on April 2, 2024

This Circular explains the following modes of collecting DST:

- Electronic Documentary Stamp Tax (eDST) System;all mandated taxpayers-users of the eDST System are required to use the eFPS in the filing of the DST declaration/return and payment of the DST

- Constructive Affixture; andapplies to private taxpayers, including eDST mandated taxpayers in case of unavailability of the eDST system, government agencies, LGUs, and other instrumentalities, whether thru manual or online filing (eFPS and eBIR Forms Package Facility)

- Purchase of loose documentary stampsaccomplished only by Special Revenue Collecting Officers/Revenue Collection Officers

Creates Alphanumeric Tax Code (ATC) for Final Withholding Tax on Gross Income Earned by Foreign Nationals Employed and Assigned in the Philippines by Offshore Gaming Licensee

Revenue Memorandum Order (“RMO”) No. 12-2024

Issued on March 25, 2024

This Order requires the use of WI750 as the ATC for gross income earned by foreign nationals or non-Filipino citizens, regardless of residency, who are employed and assigned in the Philippines by an offshore gaming license holder or its accredited service provider.

The tax rate and tax return to be used shall be 25% and BIR Form 1601-FQ/2306, respectively.

SEC Issuances

Updated Fines and Penalties on the late and non-submission of Audited Financial Statements (AFS) and General Information Sheet (GIS), and non-compliance with SEC MC 28, s. 2020

SEC Memorandum Circular (MC) No. 6-2024

Issued on March 27, 2024

The Circular imposes higher fines and penalties on the late and non-submission of AFS and GIS, and non-compliance with SEC MC 28, s. 2020.

Alternative mode for distributing and providing copies of the Notice of Meeting, Information Statement, and Other Documents in connection with the holding Of Annual Stockholders’ Meeting (“ASM”) for 2024

SEC Notice

Issued on February 23, 2024

This Notice provides that companies that would hold its Annual Stockholders Meeting for 2024 are allowed to notify their stockholders about the ASM via an alternative mode by causing the publication of the Notice of Meeting in the business section of two (2) newspapers of general circulation, in print and online format, for two (2) consecutive days; Provided that, the last publication of the Notice of Meeting (print and online) shall be made no later than twenty-one (21) days prior to the scheduled ASM.

The Notice of the Meeting shall inform the shareholders of the following:

- Date, time and place of meeting and other information as may be required under the Revised Corporation Code, other issuances of the Commission or By-laws of the Corporation; and

- The availability of an electronic copy of the Information Statement, Management Report, SEC Form 17A and other pertinent documents, as may be necessary under the given circumstance: (a) on the Company’s website; (b) and additionally, for PLCs, on the PSE Edge.

FIRB Issuances

Increasing the investment capital threshold for projects delegated to the Investment Promotion Agencies under the CREATE Act

FIRB Resolution N. 003-24

Issued on February 2, 2024

The investment capital threshold for projects delegated to the Investment Promotion Agencies shall be increased from PhP 1Billion and below to PhP 15Billion and below.

This means that only those applications for tax incentives with more than PhP 15Billion investment capital shall be subject to the approval of the FIRB Board.

RT ThinkTax

was conceptualized to provide and disseminate information on the latest news, issues and trends in the Philippines taxation.

For your comments and suggestions, please contact:

Feliza A. Peralta

Atty. Eleanor M. Montenegro

Glenn Ian D. Villanueva

Atty. William Benson S. Gan

Mary Josephine D. Tesalona

Atty. Rommel T. Geocaniga

Atty. Arvin Stephen L. Molina

Atty. Sheryl Ann Tizon-Lalucis

Joel M. Ganalon

Atty. Ryan M. Liggayu

Atty. Aemie Maria S. Jordan

Atty. Beatrice C. Aquino

Atty. Jhonnelle Mae D. Dela Paz

Atty. Ma. Carmela T. Fojas

Atty. Natasha Felicia M. Francia

Eina Elis O. Brofar

Contact us today. We’ll schedule a complimentary assessment of your company.

Let RT&Co help your business. Send your request for a proposal of services here.