RT ThinkTax

RT ThinkTax is our official monthly publication which highlights select and significant issuances and advisories of various government agencies including the BIR, SEC, BOC, FIRB, PEZA, and other regulatory bodies.

This RT ThinkTax Issue covers select, and significant issuances and advisories issued or published in January and February 2024.

BIR Issuances

Adjustment of VAT Exemption Threshold

Revenue Regulations No. 1-2024

January 15, 2024

The new price threshold for sale of house and lot and other residential dwellings for VAT-exemption purposes is PhP3,600,000.00 from the current threshold of PhP3,199,200.00.

Circularizing the Ease of Paying Taxes (EOPT) Law

Revenue Memorandum Circular (RMC) No. 3-2024

January 10, 2024

Among the salient features of the EOPT Law are as follows:

- Introduces new classification of taxpayers.

- Amends the tax base for VAT and percentage tax.

- Amends the Tax Code provisions on tax credits, refunds or tax credits of input tax, and invoicing and accounting requirements for VAT-registered persons.

- Amends the provisions on filing of returns and payment of taxes.

- Amends the compliance requirements (e.g., preservation of books of accounts and other accounting records).

- Introduces provisions on the digitalization of BIR services, as well as the EOPT and Digitalization Roadmap.

The EOPT Law took effect on January 22, 2024. However, Section 49 of the EOPT provides that with respect to the amendments to the VAT and Other Percentage Taxes, the taxpayers are given a period of six (6) months from effectivity of the implementing rules to comply.

Annual Registration Fee no longer required

RMC No. 14-2024

January 24, 2024

Effective January 22, 2024, the BIR will cease collecting the Annual Registration Fee (ARF) from business taxpayers. Business taxpayers are now exempt from filing BIR Form No. 0605 and paying the PHP 500.00 ARF for new business and annual renewal.

Existing BIR CORs that include “registration fee” under Tax Type, will retain their validity. Taxpayers may choose to update/replace their COR at their convenience. This can be done by surrendering their old COR at the RDO where they are registered on or before December 31, 2024.

Withholding Tax on Gross Remittances Made by Electronic Marketplace Operators and Digital Financial Service Providers (DFSPs)

RMC No. 8-2024

January 15, 2024

RR No. 16-2023 took effect on January 11, 2024. The e-marketplace operators and DFSPs are given a period of 90 days from the date of issuance of this circular to comply with policies or requirements of other government agencies, if any, and give them an opportunity to adjust and properly comply with RR No. 16-2023. Existing unregistered sellers/merchants shall comply with the requirements under Q4-A4 of this circular.

Branch Account Registration in Online Registration and Update System (ORUS)

RMC No. 10-2024

January 22, 2024

This circular announces the availability of branch account enrollment registration in the Online Registration and Update System (ORUS) for branches of existing taxpayers, starting January 15, 2024.

Taxpayer branches may do the following transactions in ORUS:

- Apply for Authority to Print (ATP) receipts.

- Register books of accounts

- Update the following information:

- Add registered activity/line of business.

- Add business name/trade name.

- Add tax type details/re-register tax type.

- Change registered address/apply for transfer of registration.

- Add incentives details/registration.

- Change/update contact type.

- Change/update contact person

- Enroll to Employer Services Link for the issuance of Employee TIN.

- Register a facility.

The ORUS Branch Account is separate from the Head Office’s ORUS account. Business taxpayers who want to enroll their branches must register at https://orus.bir.gov.ph/home, click New Registration and follow the succeeding instructions.

Value-Added Tax Exemption Withdrawn

RMC No. 7-2024

January 11, 2024

The following transactions under Section 109 (BB) of the Tax Code of 1997 as amended, shall no longer be exempt from VAT effective January 1, 2024:

Sale or importation of the following:

- Capital equipment, its spare parts, and raw materials, necessary for the production of personal protective equipment components such as coveralls, gown, surgical cap, surgical mask, N-95 mask, scrub suits, goggles and face shield, double or surgical gloves, dedicated shoes, and shoe covers, for COVID-19 prevention; and

- All drugs, vaccines and medical devices specifically prescribed and directly used for the treatment of COVID-19; and

- Drugs for the treatment of COVID-19 approved by the Food and Drug Administration (FDA) for use in clinical trials, including raw materials directly necessary for the production of such drugs.

Computation of surcharge for amended return in eFPS

RMC No. 9-2024

January 15, 2024

There should be no imposition of surcharge on amended tax returns, provided, that the taxpayer was able to file the initial tax return on or before the prescribed due date for its filing.

In view thereof and while the eFPS is being enhanced to adjust the computation of the surcharge, eFPS users/taxpayers are advised to disregard the surcharge computed by the system when filing an AMENDED tax return. If there is an additional tax to be paid as a result of such amendment, pay only the basic tax, the computed interest and the compromise, provided, that the original tax return was filed on or before the set deadline.

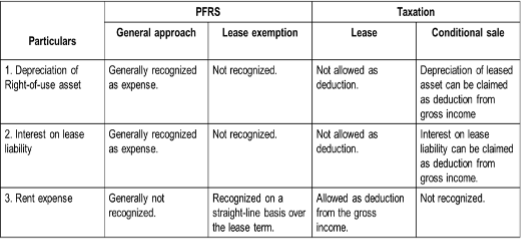

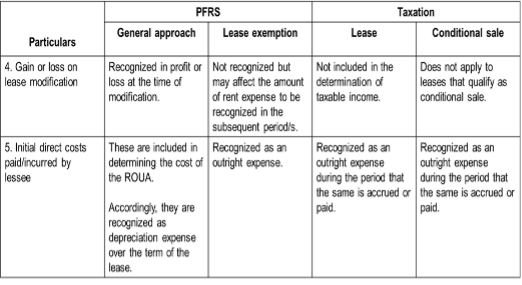

Tax Treatment of Lease Accounting by Lessees

RMC No. 11-2024

January 22, 2024

This circular provides for the following overview of PFRS and tax treatment:

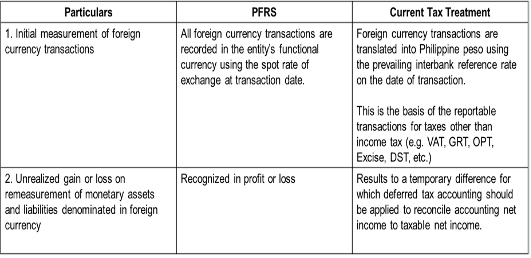

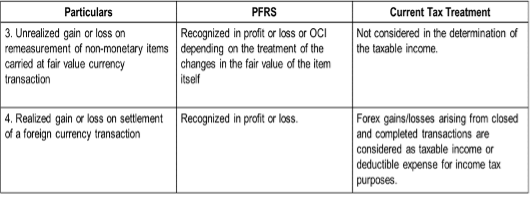

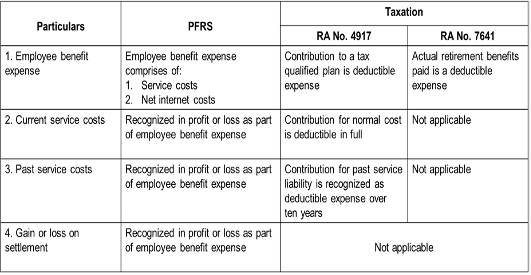

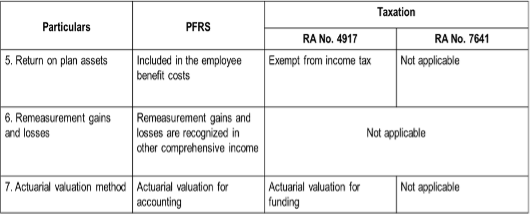

Tax Treatment of Foreign Currency Transactions

RMC No. 12-2024

January 22, 2024

Tax Treatment of Foreign Currency Transactions

RMC No. 13-2024

January 22, 2024

This circular provides for the following overview of PFRS and tax treatment:

Extending Deadline for Submission of Alphabetical List of Employees/Payees from Whom Taxes Were Withheld

RMC No. 16-2024

January 26, 2024

RMC No. 25-2024

February 13, 2024

Per RMC No. 16-2024, for taxpayers-employers who have employees availing of the 5% tax credit under the PERA Act of 2008 and who have not yet submitted their alphalists for the year 2022, the deadline shall be thirty (30) days immediately after the date of posting of a tax advisory on the BIR website announcing the availability of a separate revised data entry module.

Per RMC No. 25-2024, to provide all concerned taxpayers sufficient time to submit the alphalist for the taxable year 2023, the deadline for submission shall be thirty (30) days from the date of posting of a tax advisory on the BIR website announcing the availability of the updated version of the Alphalist Data Entry and Validation Module. In cases where alphalists were submitted using the old version, the taxpayers shall re-submit the same using the updated version upon its availability.

On February 16, 2024, the BIR posted a tax advisory announcing the availability of the updated version of the alphalist data entry and validation module (version 7.2) which can be downloaded from the BIR website (www.bir.gov.ph) and which includes the 5% tax credit incentive under RA No. 9505 or the PERA Act of 2008 and the revised income tax rates for TY 2023 under the TRAIN Law.

Tax Treatment of Interest Expense

RMC No. 19-2024

February 5, 2024

This RMC clarifies the tax treatment of interest expense paid or incurred on indebtedness in connection with the taxpayer’s profession, trade or business and other related matters.

The Table below shows the differences between the accounting treatment and current tax treatment on interest expenses.

| Particulars | Accounting Treatment | Current Tax Treatment |

|---|---|---|

| Interest expense on borrowing arrangements | Interest is recognized as an expense using the effective interest method. Interests incurred directly attributable to the acquisition of a qualifying asset are capitalized as part of the cost of the asset. | Interest can be claimed as a deduction, subject to certain limitations, provided all the criteria are met. Interest incurred to acquire property used in trade, business or exercise of profession may be recognized as an expense in the year incurred or capitalized as part of the cost of the property. |

| Interest paid in advance by the taxpayer reporting income on cash basis | Interest is recognized as an expense when incurred. | Interest can be claimed as a deduction in the year the indebtedness is paid. If the indebtedness is payable in periodic amortizations, the amount of interest which corresponds to the amount of the principal amortized or paid during the year shall be allowed as deduction in such taxable year. |

| Interest expense on indebtedness between related parties | Interest expense is recorded when incurred. | Interest expense is not deductible pursuant to Section 34(B)(2)(b) of the National Internal Revenue Code of 1997, as amended. |

Updated Checklist of Requirements for Frontline Services

RMC No. 27-2024

February 20, 2024

This RMC circularizes the updated Checklist of Documentary Requirements for BIR registration-related frontline services. The checklists are annexed to the RMC. The RMC states that the BIR shall only process applications or requests with complete documentary requirements and shall not process deficient or incomplete applications or requests, pursuant to the Ease of Doing Business and Efficient Government Delivery Act of 2018.

RT ThinkTax

was conceptualized to provide and disseminate information on the latest news, issues and trends in the Philippines taxation.

For your comments and suggestions, please contact:

Feliza A. Peralta

Atty. Eleanor M. Montenegro

Glenn Ian D. Villanueva

Atty. William Benson S. Gan

Mary Josephine D. Tesalona

Atty. Rommel T. Geocaniga

Atty. Arvin Stephen L. Molina

Atty. Sheryl Ann Tizon-Lalucis

Joel M. Ganalon

Atty. Ryan M. Liggayu

Atty. Aemie Maria S. Jordan

Atty. Beatrice C. Aquino

Atty. Jhonnelle Mae D. Dela Paz

Atty. Ma. Carmela T. Fojas

Atty. Natasha Felicia M. Francia

Eina Elis O. Brofar

Contact us today. We’ll schedule a complimentary assessment of your company.

Let RT&Co help your business. Send your request for a proposal of services here.